Navigating the financial landscape of memory care can be a daunting task, but it is crucial for families to explore all available options to ensure their loved ones receive the best possible care. Memory care communities, often situated within assisted living facilities or nursing homes, offer specialized services for individuals with Alzheimer’s disease, dementia, or other cognitive impairments. The cost of these services varies widely based on factors such as the level of care required, geographic location, and the size of the living space.

While insurance can play a role, it is just one piece of the puzzle. Medicaid, Medicare, private pay, and other government financial assistance programs like veteran benefits are also important considerations. Understanding these costs and payment methods can help families make informed decisions. By leveraging all available funding options, families can manage the financial burden and ensure their loved ones remain healthy, safe, and engaged in their memory care communities. 1,2

Understanding Memory Care Costs

The expenses involved in memory care can be extensive, covering a range of services from housing to medical and personal support. Typically, memory care units charge a base monthly fee that includes a shared or private room, three meals per day, snacks, planned social activities, and 24/7 emergency assistance. However, additional fees often apply for personal care services, such as medication administration and help with activities of daily living (ADLs) like bathing and dressing. In nursing homes, an all-inclusive monthly fee generally covers these services. It’s crucial for families to inquire about what is included in the base fee when touring memory care communities, as these additional costs can add up quickly. 1

In addition to levels of care, geography can significantly impact the overall cost of memory care. In high-cost living areas like New York and San Jose, memory care expenses are substantially higher compared to regions with lower living costs such as Houston and Phoenix. State licensing requirements for memory care facilities, which dictate standards for living space, personnel, and supervision, also influence costs. Additionally, the availability of memory care options varies throughout the United States, with smaller states potentially having fewer, more expensive communities. Therefore, understanding the geographical cost variations and specific state requirements is essential for families planning for memory care expenses. 3

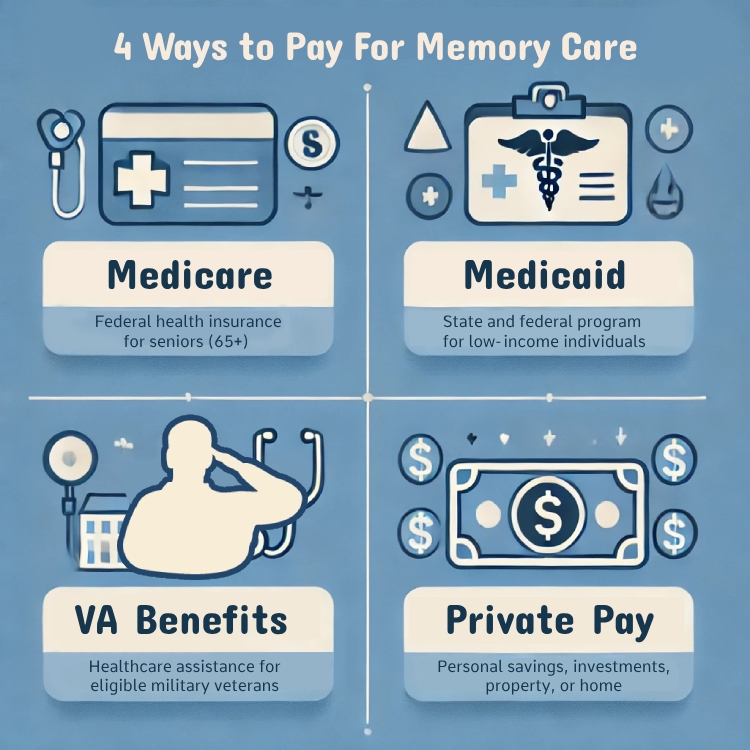

Ways to Pay for Memory Care

When it comes to financing memory care, understanding the various payment options is necessary. The main avenues to consider are Medicare, Medicaid, VA benefits, insurance and private pay.

Medicare

Medicare Coverage: Available to those over 65, Medicare includes inpatient hospital care, some medical fees, and certain medical items. Medicare Part D covers many prescription drugs. While Medicare can pay for up to 100 days of in-home care, it doesn’t cover long-term nursing home care. It does, however, pay for an annual wellness visit and a cognitive assessment and care plan service, which can be beneficial for Alzheimer’s patients. 3

Medicare Advantage Plans: These plans, particularly Special Needs Plans, cater to individuals with chronic conditions like dementia. They cover everything that Original Medicare covers, plus additional services focused on dementia care. These plans might require both Medicare and Medicaid coverage or nursing care and often cover a specific geographic area. Although they may cost more than Original Medicare, they can be cost-effective compared to the combined costs of Medicare premiums, Medigap policies, and Part D plans. 3

Medicaid

Medicaid Eligibility: Medicaid is a state-governed program that can help pay for memory care for Medicaid-eligible older adults living with dementia. It typically covers the full cost of care in nursing homes. In assisted living or memory care communities, Medicaid can be used in combination with Medicaid waiver programs to help cover costs. 1

Medicaid Waiver Programs: States tailor these programs to meet residents’ needs. The United States has over 250 Home & Community-Based Services (HCBS) waiver programs, which can help pay for memory care outside of nursing homes. Checking with your state’s Medicaid agency or a Medicaid adviser through the local area agency on aging can provide specific information. 1

Veteran’s Benefits

Veteran-Directed Care (VDC): This program provides a monthly budget for veterans or their caregivers, covering personal care services, home modifications, adult day care, and more. Veterans can manage their budget and choose services that best fit their needs. 2

Aid and Attendance Benefit: This additional monetary benefit can be added to a VA pension to help cover the cost of assisted living, memory care, skilled nursing, and in-home medical care services. Eligibility requires needing assistance with ADLs, being bedridden, residing in a nursing home, or having severe visual impairment. 2

VA Dependent Parent Benefit: This needs-based cash benefit helps veterans caring for a parent with dementia. It’s available to veterans receiving disability compensation or VA educational benefits and has no income restrictions. 2

State Veterans Homes: These long-term care facilities, funded by the VA but run by states, offer nursing home care, memory care, assisted living, and adult day care. 2

Private Pay

Personal Savings and Investments: Many families use personal savings, investments (such as stocks, bonds, and real estate), a life insurance policy, and personal property (such as jewelry or artwork) to pay for memory care. 4

Selling or Renting a Home: If the homeowner no longer needs residence, selling or renting a property can generate substantial funds to directly cover memory care expenses either in a lump sum or as a steady stream of income. 2

Reverse Mortgages: For those aged 62 or older, a reverse mortgage allows homeowners to convert home equity into cash while retaining homeownership. This can provide a significant source of income for memory care without affecting Social Security or Medicare benefits, although it may impact eligibility for other government programs. 4

Insurance

Long-Term Care Insurance: This type of insurance is specifically designed to cover long-term care costs, including memory care in nursing homes or specialized medical care facilities. Policies vary, so it’s essential to review the specific benefits and coverage details.

Private Health Insurance: For those younger than 65, private insurance, group employee plans, or retiree health coverage might be available. These plans can help cover some costs associated with dementia care, but coverage specifics will depend on the individual policy.

Social Security Disability Insurance (SSDI): Eligible individuals with dementia may qualify for SSDI, which can help cover memory care costs. This requires a thorough review of the impairments and their impact on the individual’s ability to work. 3

Combining various financial strategies is essential for managing the costs of memory care effectively. Utilizing insurance, Medicaid, Medicare, and private pay options can provide comprehensive coverage for necessary services. Families must explore all available options when creating a personalized financial plan tailored for a family member’s needs.

Family Involvement

Engage the family in providing care and covering costs. For example, a grandchild could live with the patient to offer limited assistance and oversight for mild memory issues. Another option is for the patient to move back in with their children or into an in-law suite, particularly for families with larger homes and a cultural obligation to care for elderly parents. The family and the resident can discuss and develop a mutually beneficial strategy for support and care when possible.

By starting early and understanding each funding source, families can ensure their loved ones receive quality care without excessive financial strain. Planning ahead and leveraging these resources can make a significant difference in accessing and affording the best memory care available.

References

[1] Dis, Kate Van. “The Cost of Memory Care: What to Expect.” NCOA Adviser, National Council on Aging, 22 Feb. 2024, www.ncoa.org/adviser/local-care/memory-care-costs/.

[2] Behrman, Haleigh. “How to Pay for Memory Care: Surprising Tips for Families.” How to Pay for Memory Care | A Place for Mom, www.aplaceformom.com/caregiver-resources/articles/how-to-pay-memory-care. Accessed 17 May 2024.

[3] “Paying for Alzheimer’s Care.” MemoryCare.Com, 19 Apr. 2024, www.memorycare.com/paying-for-alzheimers-care/.

[4] “Paying for Care.” Alzheimer’s Disease and Dementia, www.alz.org/help-support/caregiving/financial-legal-planning/paying-for-care. Accessed 17 May 2024.

The information provided in the article is for general informational purposes only. This information is not a substitute for medical advice. Accordingly, before taking any actions based upon such information, you are encouraged to consult with the appropriate professionals.